Sinology: A Year of Living Less Dangerously

By Andy Rothman

The publication this week of the U.S. — China trade deal and the final macro numbers for 2019 should set the stage for healthy economic performance and stronger market sentiment in China in 2020, but the risk of a return to tense relations between Washington and Beijing looms over 2021 and beyond.

The “phase one” trade deal should create a truce in the tariff dispute. President Trump appears to believe that declaring victory over China will boost his re-election prospects, and it seems that Xi Jinping is willing to cooperate. There are no signs, however, that the Trump administration will scale back its willingness to confront Xi on a range of issues, especially those related to technology competition. The resulting political tension, as well as the deal's unrealistically high purchasing targets, could break the truce in 2021.

Headline writers will continue to focus on slower year-on-year (YoY) growth rates in China, but most investors understand that the base effect allows the economy to expand by far more today than at the faster speeds of a decade ago. This creates greater opportunity for Chinese firms selling goods and services to local consumers, as well as for investors in those firms.

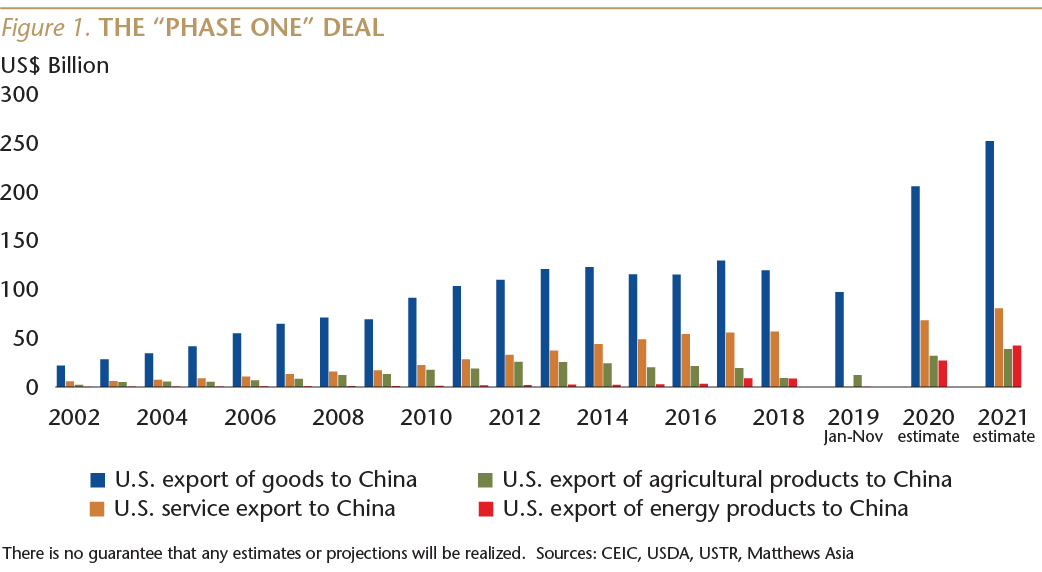

Assessing the trade deal

The trade deal will likely accomplish Trump's main objective: creating the appearance of an important accomplishment as the election approaches. But the deal did not create effective new solutions to most of the trade-related problems cited when the tariffs were launched.

On intellectual property issues, a Trump administration priority, the deal accomplishes little. Many specific steps in the agreement were previously announced by Beijing, and the new steps are incremental. Most importantly, the agreement does not require China to make legal and structural changes needed to ensure compliance. There also were no significant new commitments on exchange-rate management or industrial policy.

Overall, this deal is not a significant improvement over the Trans-Pacific Partnership (TPP) program cancelled by the Trump administration, or the draft bilateral investment treaty (BIT) with China that was negotiated by the Obama administration but abandoned by Trump.

The deal also leaves in place much of the tariff burden already borne by American companies and consumers. “Even after the deal goes into effect, Trump's tariffs will still cover nearly two-thirds of all U.S. imports from China,” according to Chad Brown of the Peterson Institute for International Economics. “He will also have increased the average U.S. tariff on imports from China to 19.3%, as compared to 3%” before the dispute began.

The 2020 deal upside

There are important positive consequences of the deal. I think Trump wants the deal to succeed to boost his re-election prospects—and Beijing seems willing to cooperate—so the trade truce is likely to hold at least through November. By significantly reducing the risk of the tariff dispute escalating into a full-blown trade war, the deal is likely to boost sentiment among Chinese companies and global equity and bond investors who are thinking about increasing their China exposure.

The 2021 deal risks

Two things could derail the trade truce next year. First, there are as yet no signs that the Trump administration will scale back its campaign to confront Xi on a broad range of issues, especially those related to technology competition. By next year, it is possible that Xi may reconsider whether cooperating with Trump on trade makes sense at a time when Washington is taking a confrontational approach on most other issues. Of course, if there is a new American president next year, Beijing will wait to see how that administration approaches the relationship with China.

My second concern is that the deal calls for what I believe are unrealistically large increases in Chinese imports from the U.S. According to the terms of the deal, in 2020, China's overall imports from the U.S. should increase by 50% over the 2017 baseline, and then increase by another 20% YoY in 2021, for a total two-year increase of US$200 billion. This includes increases over the 2017 baseline of 52% for agricultural and 257% for energy imports in 2020, and then further increases in 2021—19% YoY for agriculture and 60% YoY for energy.

There is, of course, room for the Trump administration to play with the numbers. The text of the deal states, for example, that aircraft orders as well as deliveries will count toward the Chinese commitment, so Beijing could sign a lot of contracts for possible later delivery to inflate the numbers. But this kind of thing will only work if both governments cooperate. As U.S. Trade Representative Robert Lighthizer acknowledged, “This deal will work if China wants it to work.” And if, after the election, the Trump (or a different) administration also wants it to work.

As an aside, the deal text includes a long list of goods that are targeted for increases to hit China's import targets. Some of them are puzzling. Iron and steel, for example, are on the list, even though in 2017, the U.S. exported less than US$500 million worth of that to China. Also on the list: “perfumes and toilet waters”; “preparations for use on the hair”; and “tea, whether or not flavored.” (Yes, China is the world's largest producer of tea.)

Yes, Virginia, China's growth rate is decelerating

As we switch to the topic of China's economic health, I want to start by addressing the headline writers who pointed out that last year's GDP growth rate was the slowest since the Tang dynasty. I'd like to suggest another perspective.

China's growth has been decelerating gradually for over a decade, but the size of the economy (the base) has expanded quite a bit. GDP growth was 9.4% a decade ago, but the base for last year's 6.1% GDP growth was 188% larger than the base 10 years ago, meaning the incremental expansion in the size of China's economy in 2019 was 145% bigger than it was at the faster growth rate a decade ago. In other words, there was a greater opportunity last year for Chinese companies selling goods and services to Chinese consumers than compared to 10 years ago, when the GDP growth rate was much faster.

I expect that the YoY growth rates of most aspects of the Chinese economy will continue to decelerate, and as long as that deceleration continues to be gradual, I do not expect panic from the Chinese government, or from investors.

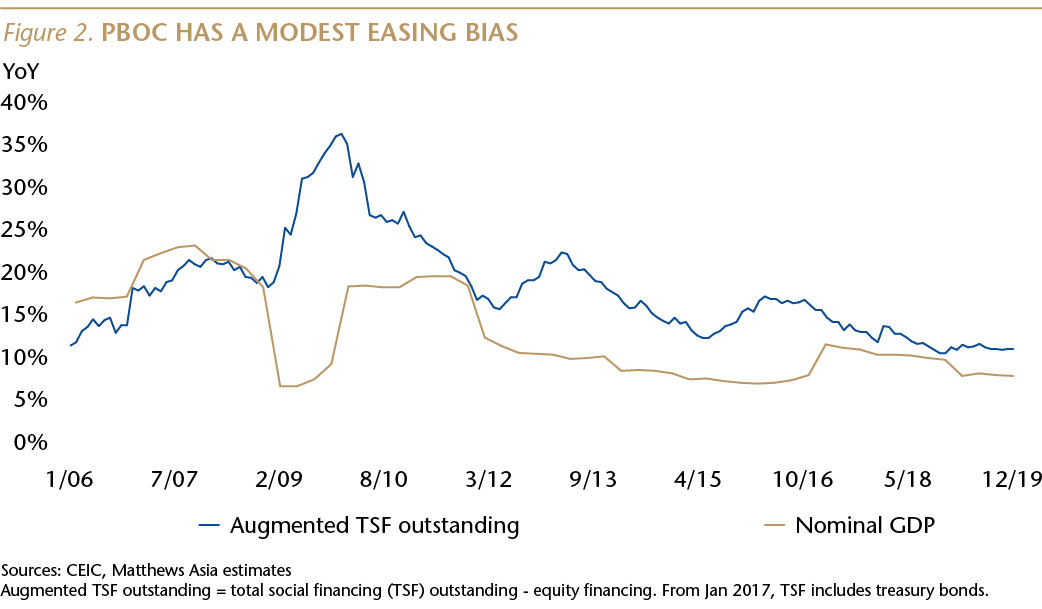

Modest easing of monetary policy

A clear sign that the government has been relatively comfortable with the health of the economy is that there has been only modest easing of monetary policy. I expect that approach to continue in 2020. The focus will be on stabilizing growth in response to slower global demand, not an effort to reaccelerate growth.

As was the case last year, aggregate credit outstanding (augmented Total Social Finance) will likely expand just a bit faster than nominal GDP growth, but not to the extent in past years.

Derisking to continue

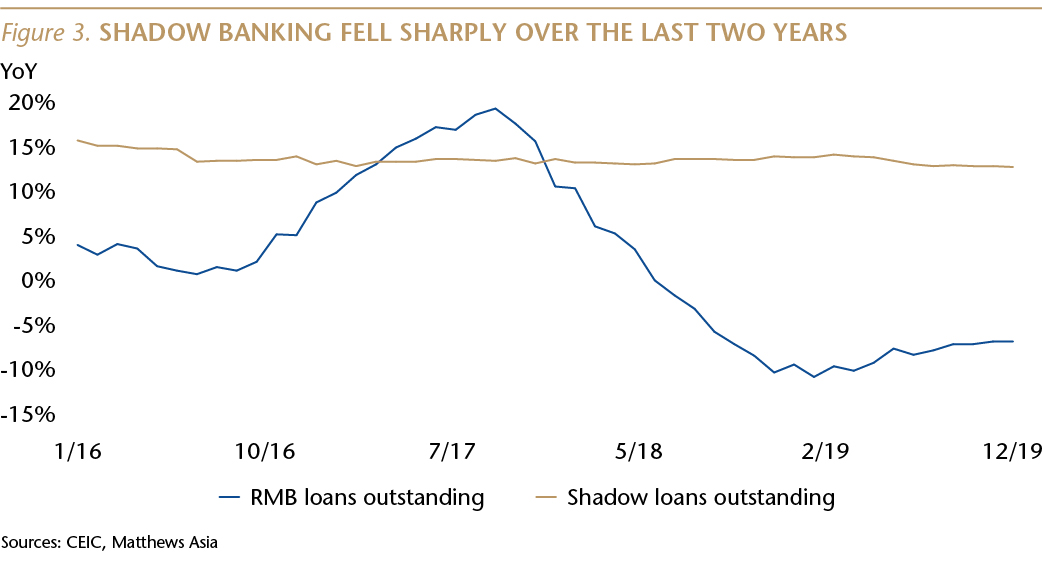

I also anticipate that the government will continue to take steps to reduce financial sector risks this year. As I wrote last month, I expect further consolidation of smaller banks. I also expect a continuation of last year's experiments of selected defaults by state-owned and private firms, in an effort to push investors to price risk. I do not expect the government to relax their tight controls over off-balance-sheet (shadow) financial activity.

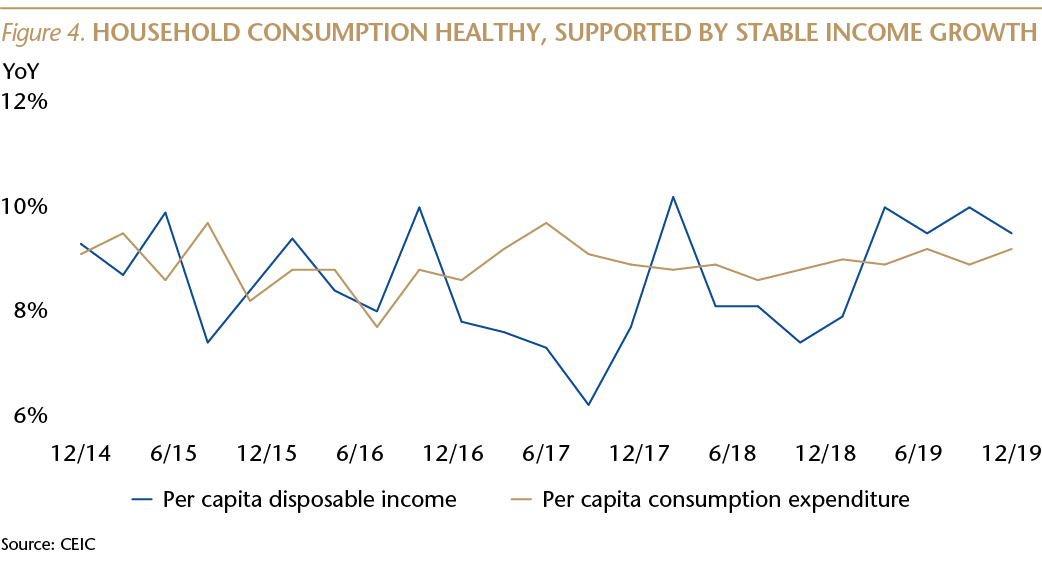

Likely to remain the world's best consumer story

China's consumers drove economic growth again in 2019, and I expect that to continue in 2020. Last year was the eight consecutive year in which the consumer and services (or tertiary) part of GDP was the largest part, and consumption accounted for 58% of GDP growth.

Strong income growth continues to fuel the consumer story. Nominal per capita disposable income rose 9.1% in 4Q19, up from 8.5% a year earlier and 9% two years ago.

Household consumption spending rose 9.4% YoY in 4Q19, compared to 8% a year earlier and 6.1% two years ago. This metric for consumer spending, which is published quarterly, includes a wider range of services compared to the retail sales data. Services now account for about 46% of household consumption.

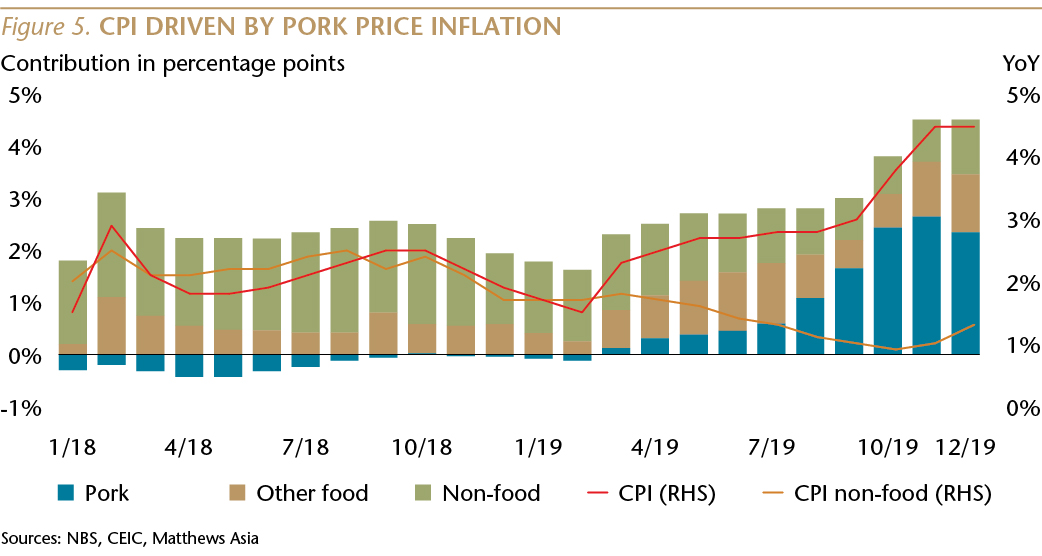

Pork prices should ease, so inflation shouldn't be a big problem

An outbreak of African Swine Fever decimated China's hog population last year, which pushed up the price of pork—the country's primary protein source. Headline CPI rose to 4.5% last month and will remain elevated this year, driven entirely by pork. The disease seems to be fading and pork prices stabilized recently, although there is likely to be another spike in January, as the Lunar New Year holiday boosts demand. Core inflation, which was 1.4% YoY in December, should remain low, and I do not expect inflation to have a significant impact on consumer sentiment.

Modest improvement in CapEx likely

Investment spending by private firms was weak last year, largely due to uncertainty resulting from the Trump tariff dispute. The signing on Wednesday of the trade deal is likely to reduce that uncertainty, leading to a modest pickup in CapEx spending. Only modest, because the risk of a return to higher U.S. — China tensions in 2021 remains.

Regards,

Andy Rothman

Investment Strategist

Matthews Asia

Back to Thought Leadership